US Stocks

US Stocks US Options

US Options Emerging Asia

Emerging Asia GBP Cash Savings

GBP Cash Savings Charts & Tools

Charts & Tools Paper Trading

Paper Trading Extended Hours

Extended Hours Wall Street Journal

Wall Street JournalW. P. Carey Inc.'s (NYSE:WPC) Stock is Soaring But Financials Seem Inconsistent: Will The Uptrend Continue?

W. P. Carey's (NYSE:WPC) stock is up by a considerable 11% over the past three months. However, we decided to pay attention to the company's fundamentals which don't appear to give a clear sign about the company's financial health. Specifically, we decided to study W. P. Carey's ROE in this article.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. In simpler terms, it measures the profitability of a company in relation to shareholder's equity.

Check out our latest analysis for W. P. Carey

How Is ROE Calculated?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for W. P. Carey is:

5.5% = US$461m ÷ US$8.4b (Based on the trailing twelve months to December 2024).

The 'return' refers to a company's earnings over the last year. That means that for every $1 worth of shareholders' equity, the company generated $0.05 in profit.

What Has ROE Got To Do With Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

W. P. Carey's Earnings Growth And 5.5% ROE

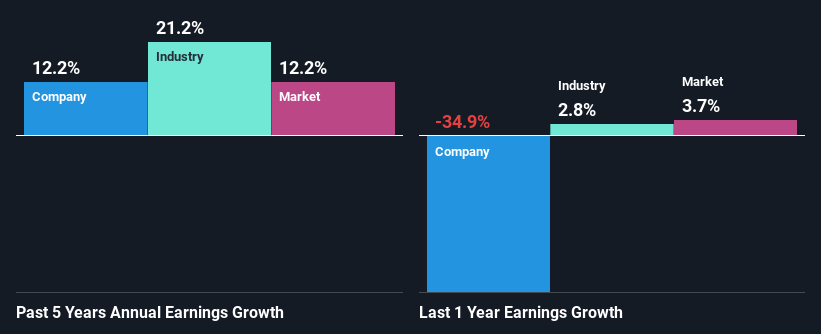

On the face of it, W. P. Carey's ROE is not much to talk about. However, given that the company's ROE is similar to the average industry ROE of 5.5%, we may spare it some thought. Even so, W. P. Carey has shown a fairly decent growth in its net income which grew at a rate of 12%. Given the slightly low ROE, it is likely that there could be some other aspects that are driving this growth. For example, it is possible that the company's management has made some good strategic decisions, or that the company has a low payout ratio.

Next, on comparing with the industry net income growth, we found that W. P. Carey's reported growth was lower than the industry growth of 21% over the last few years, which is not something we like to see.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. Is WPC fairly valued? This infographic on the company's intrinsic value has everything you need to know.

Is W. P. Carey Efficiently Re-investing Its Profits?

W. P. Carey has a high three-year median payout ratio of 81%. This means that it has only 19% of its income left to reinvest into its business. However, it's not unusual to see a REIT with such a high payout ratio mainly due to statutory requirements. Despite this, the company's earnings grew moderately as we saw above.

Moreover, W. P. Carey is determined to keep sharing its profits with shareholders which we infer from its long history of paying a dividend for at least ten years. Our latest analyst data shows that the future payout ratio of the company is expected to rise to 132% over the next three years. However, W. P. Carey's future ROE is expected to rise to 7.9% despite the expected increase in the company's payout ratio. We infer that there could be other factors that could be driving the anticipated growth in the company's ROE.

Conclusion

Overall, we have mixed feelings about W. P. Carey. While the company has posted a decent earnings growth, We do feel that the earnings growth number could have been even higher, had the company been reinvesting more of its earnings at a higher rate of return. With that said, the latest industry analyst forecasts reveal that the company's earnings are expected to accelerate. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.