US Stocks

US Stocks US Options

US Options Emerging Asia

Emerging Asia GBP Cash Savings

GBP Cash Savings Charts & Tools

Charts & Tools Paper Trading

Paper Trading Extended Hours

Extended Hours Wall Street Journal

Wall Street JournalMP Materials (NYSE:MP) Stock Surges 60% As Sales Jump To US$61 Million

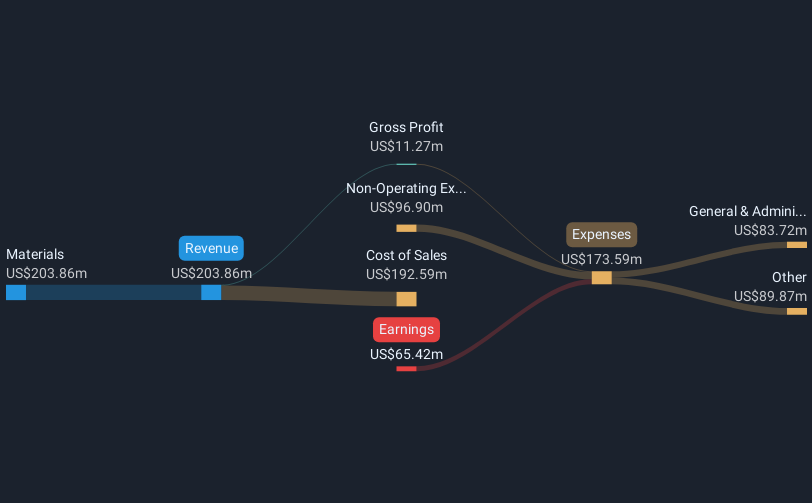

MP Materials (NYSE:MP) recently reported its fourth-quarter results, with sales increasing to $61 million from $41 million year-over-year, alongside a net loss of $22 million, compared with $16 million previously. Despite these figures reflecting a broader net loss, the company's stock price surged by 60% over the last quarter, a promising move for shareholders. The higher REO and NdPr production volumes reported suggest robust operational efficiency that might have positively influenced the stock performance. Additionally, the successful progress of MP's ambitious goals in the U.S. rare earth magnet supply chain possibly signaled improved strategic positioning to investors. While the broader market showed restrained gains, MP's significant stock price appreciation suggests investor optimism potentially buoyed by these production and strategic achievements against the backdrop of an otherwise uncertain market environment.

Buy, Hold or Sell MP Materials? View our complete analysis and fair value estimate and you decide.

Over the past year, MP Materials’ total shareholder return reached 105.12%, markedly outperforming both the US market, which returned 10%, and the US Metals and Mining industry, which saw a 4.7% rise. This impressive performance is anchored in key developments. Notably, the company executed a significant share buyback program, repurchasing 15.25 million shares, amounting to 8.66% of outstanding shares, valuing at US$225.03 million. This likely contributed to bolstering investor confidence and supporting share price appreciation.

Further underpinning gains, MP’s operational strides were evident in increased REO and NdPr production volumes in Q4 2024. Production saw rises from 9,257 metric tons to 11,478 metric tons and from 150 metric tons to 413 metric tons, respectively, over the past year. While the company remains unprofitable, this operational efficiency likely coupled with future growth expectations could resonate positively with investors, explaining strong shareholder returns despite broader profit challenges.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com