US Stocks

US Stocks US Options

US Options Emerging Asia

Emerging Asia GBP Cash Savings

GBP Cash Savings Charts & Tools

Charts & Tools Paper Trading

Paper Trading Extended Hours

Extended Hours Wall Street Journal

Wall Street Journal3 Undiscovered Gems In The US Market To Enhance Your Portfolio

Over the last 7 days, the United States market has remained flat, yet it is up 8.1% over the past year with earnings expected to grow by 14% per annum in the coming years. In such a dynamic environment, identifying stocks that offer unique growth potential while complementing existing portfolio strategies can be key to capitalizing on these market conditions.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Morris State Bancshares | 9.72% | 4.93% | 6.51% | ★★★★★★ |

| Wilson Bank Holding | NA | 7.87% | 8.22% | ★★★★★★ |

| Oakworth Capital | 31.49% | 14.78% | 4.46% | ★★★★★★ |

| ASA Gold and Precious Metals | NA | 7.47% | -26.86% | ★★★★★★ |

| Omega Flex | NA | -0.52% | 0.74% | ★★★★★★ |

| Teekay | NA | -0.89% | 62.53% | ★★★★★★ |

| Anbio Biotechnology | NA | 8.43% | 184.88% | ★★★★★★ |

| FRMO | 0.08% | 38.78% | 45.85% | ★★★★★☆ |

| Pure Cycle | 5.15% | -2.61% | -6.23% | ★★★★★☆ |

| Reitar Logtech Holdings | 31.39% | 231.46% | 41.38% | ★★★★☆☆ |

Let's uncover some gems from our specialized screener.

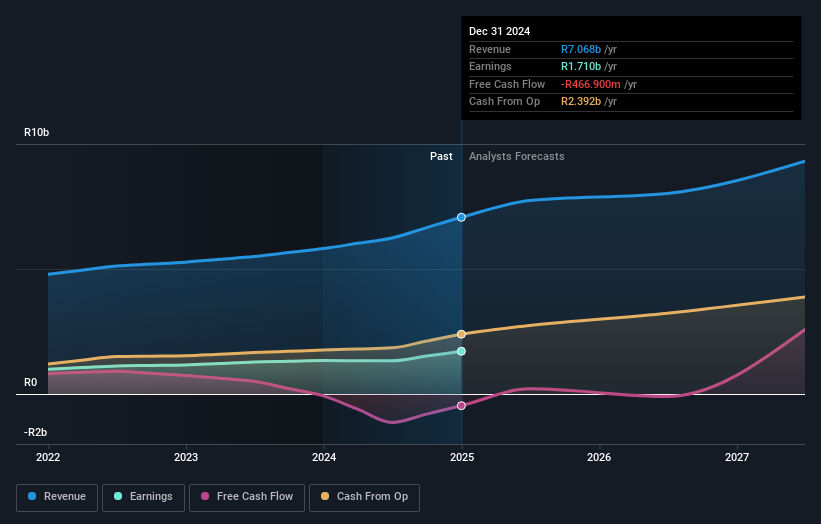

Karooooo (NasdaqCM:KARO)

Simply Wall St Value Rating: ★★★★★☆

Overview: Karooooo Ltd. operates a mobility software-as-a-service platform for connected vehicles across multiple regions, including South Africa, Europe, and the United States, with a market capitalization of $1.33 billion.

Operations: The company's revenue primarily comes from its Cartrack segment, generating ZAR 3.99 billion, and Karooooo Logistics, contributing ZAR 403.12 million. The net profit margin is a key financial metric to consider for evaluating the company's profitability trends over time.

Karooooo, a promising player in fleet management SaaS, has demonstrated strong financial performance with earnings growing at 24.4% annually over the past five years. Despite a debt-to-equity increase from 7.8% to 13%, the company maintains more cash than total debt, ensuring financial stability. Recent Q3 results show sales of ZAR 1,159 million and net income of ZAR 237 million, reflecting robust growth compared to last year. With a P/E ratio of 27.6x below industry average and expansion into Southeast Asia and Europe underway, Karooooo is poised for further growth despite potential short-term profitability challenges due to expansion costs.

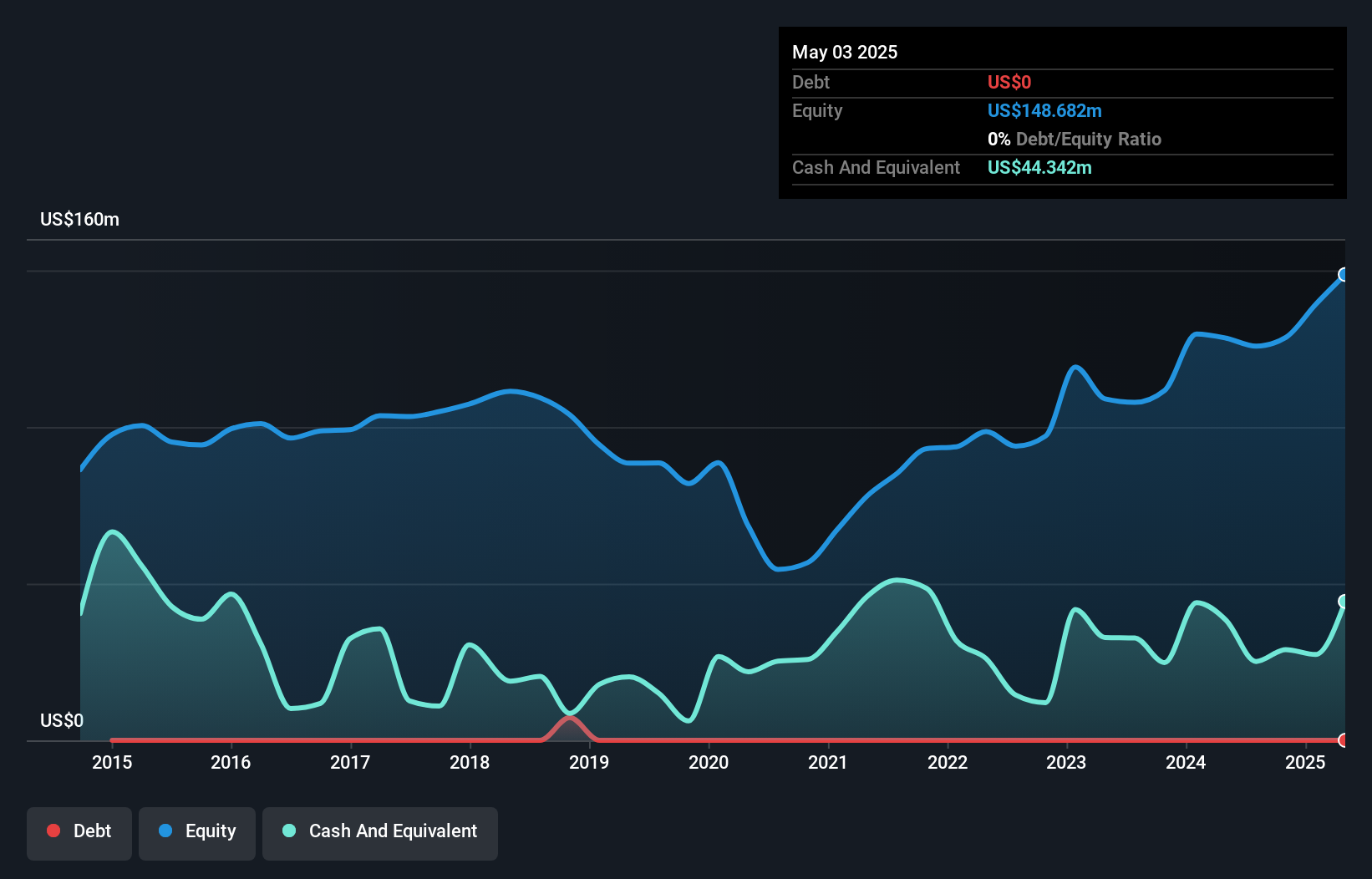

Build-A-Bear Workshop (NYSE:BBW)

Simply Wall St Value Rating: ★★★★★★

Overview: Build-A-Bear Workshop, Inc. is a multi-channel retailer specializing in plush animals and related products with operations in the United States, Canada, the United Kingdom, Ireland, and internationally; it has a market cap of $491.02 million.

Operations: The company's primary revenue stream comes from its retail segment, generating $460.33 million, followed by commercial sales at $31.39 million and international franchising at $4.69 million.

Build-A-Bear Workshop, a notable player in the experiential retail space, is leveraging its debt-free status and high-quality earnings to expand internationally. The company plans to open 50 new stores in 2025, focusing on tourist hotspots and international markets. Despite facing inflationary pressures and potential e-commerce slowdowns, Build-A-Bear's recent share repurchase of 288,273 shares for US$6.6 million highlights confidence in its value proposition. With a current share price of US$35.99 and an analyst target of US$54.33, there's room for growth if challenges like tariff impacts are managed effectively.

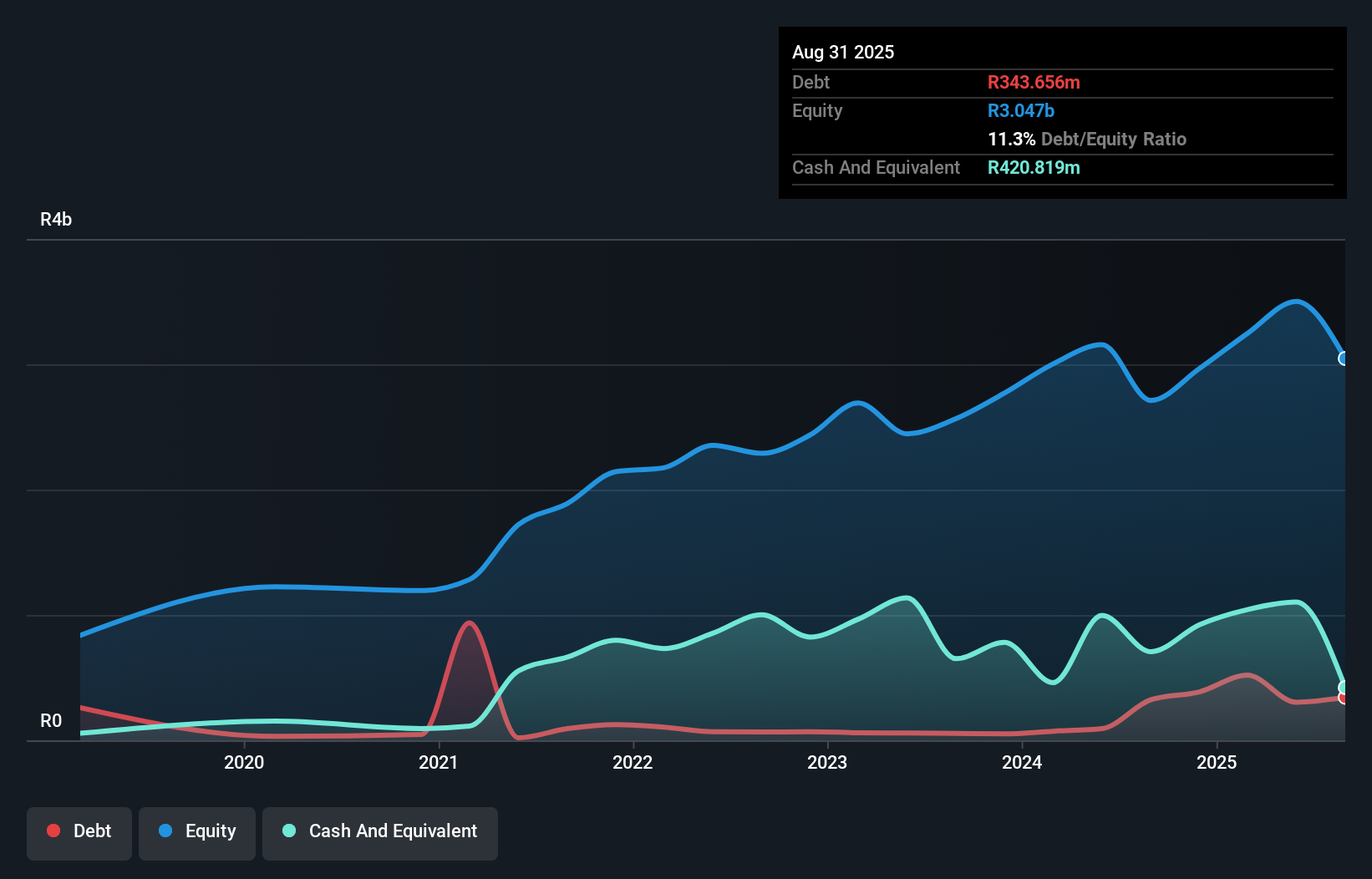

DRDGOLD (NYSE:DRD)

Simply Wall St Value Rating: ★★★★★☆

Overview: DRDGOLD Limited is a South African gold mining company focused on extracting gold from surface mine tailings, with a market capitalization of approximately $1.23 billion.

Operations: DRDGOLD generates revenue primarily from two segments: Ergo, contributing ZAR 5.05 billion, and FWGR, with ZAR 2.02 billion.

DRDGOLD, a player in the mining sector, showcases a robust financial profile with earnings surging by 28% over the past year, outpacing the industry average. Despite not generating positive free cash flow recently, its debt-free status and high-quality non-cash earnings provide stability. The company reported gold production of 82,434 ounces for the half-year ending December 2024 and announced an interim dividend of 30 SA cents per share. Trading at about 82% below its estimated fair value suggests potential upside. Revenue is expected to grow nearly 10% annually, indicating promising future prospects in a competitive market.

- Delve into the full analysis health report here for a deeper understanding of DRDGOLD.

Gain insights into DRDGOLD's past trends and performance with our Past report.

Taking Advantage

- Investigate our full lineup of 283 US Undiscovered Gems With Strong Fundamentals right here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com